The UK forms approximately 5% of global equity markets by capitalisation, but for home investors it forms a significant part of most portfolios, with a lot of the largest British companies playing major roles in the global economy.

But what are the material ESG risks the UK equity market is exposed to as a whole? Topics that tend to be at the forefront of ESG thinking centre on fossil fuels, pollution and business scandals, but are these the largest exposures from a financial materiality perspective? Let’s take a look at the overall UK equity market, it’s industry groups and their ESG risks through a simple mapping exercise.

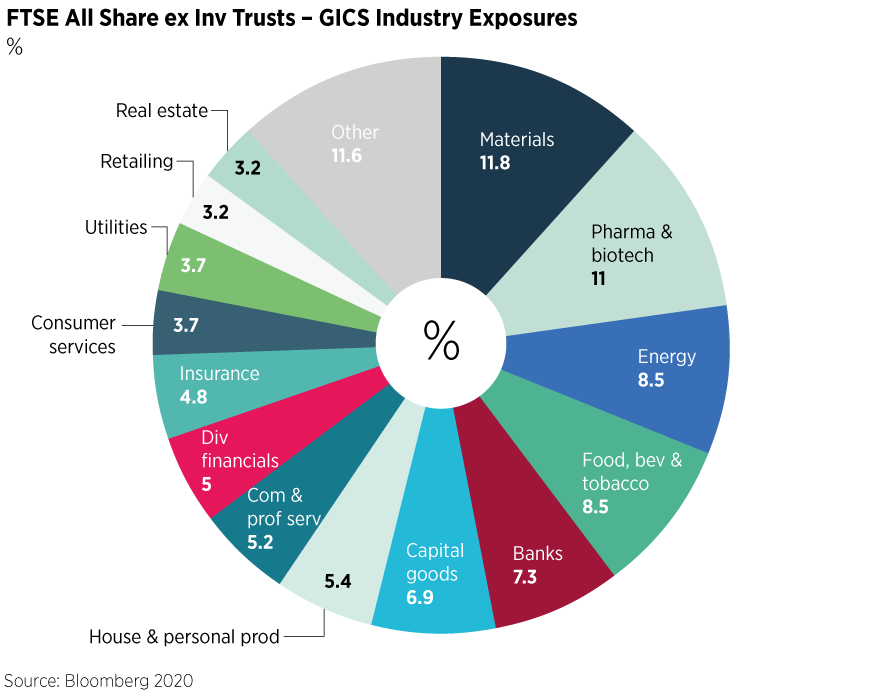

Taking the FTSE All-Share index excluding investment trusts as a representation of the UK market, we look at the material ESG issues across major industries. The index represents the performance of all eligible companies listed on the London Stock Exchange main market, capturing 98% of the UK’s market capitalisation.

Determining which ESG issues are most material is not an exact science, and there is a degree of subjectivity with differences between what different investors consider significant when analysing companies and industries. Typically, this is because materiality is based on a forecast or judgement of how much a given ESG issue will impact a company’s financial metrics such as future cashflow.

See also: – ESG factors: A forecaster of disaster?

Let’s take the SASB (Sustainability Accounting Standards Board) Materiality Map, a framework that focuses on material issues that are reasonably likely to impact the operating performance of companies across industries and map it to industry groups of the FTSE All-Share. The relevance of ESG issues naturally vary from industry to industry, for example, fuel efficiency will have a bigger impact on the carbon footprint and P/L of an airline than it does for a retail bank.

Materiality maps take this into consideration, looking at the management of corporations’ environmental and social impacts arising from production of goods and services alongside the impacts that sustainability challenges have on innovation, business models, and corporate governance, and vice versa. The map covers 26 sustainability topics organised under 5 broad ESG dimensions – Environment, Social Capital, Human Capital, Business Model and Innovation, and Leadership and Governance.

The FTSE All0-Share is relatively well diversified, with the largest industry exposures in Materials, Pharma & Biotech and Energy. With a 12% allocation, the Materials industry group covers several different sub-sectors ranging from Chemicals to Commodity miners. Along with a 10% exposure to Energy, the level of extractive sub-industries is considerable. Already with over 20% exposure to environmentally intensive sub-industries it would be natural to think that environmental issues are of most materiality to the All-Share. To see if this is the case, we take the weight in each GICS industry group within the All-Share index and map them across the 26 sustainability-related issues and calculate the index exposure to each issue in a cap-weighted manner.

The results are interesting, given the relative dominance of E within the sphere of ESG thinking. After mapping all industry group weightings to their SASB category exposures, we find that the material dimension that the All-Share is most exposed to is Social Capital. SASB defines this dimension to include issues that affect the productivity of employees, management of labour relations, health and safety of employees along with the ability to create a safety culture.

See also: – Nutmeg: Social concerns top ESG investors’ reasons to divest

On a cap-weighted basis, 96% of the All-Share is exposed to this material issue, followed by 90% in Business Model and Innovation, which focuses on the integration of ESG issues in a company’s value creation process. In terms of materiality exposure, Environment ranks last, but still a significant exposure in excess of 50%. It should be noted that materiality issues are non-mutually exclusive, therefore multiple sustainability issues can be material to any given sector.

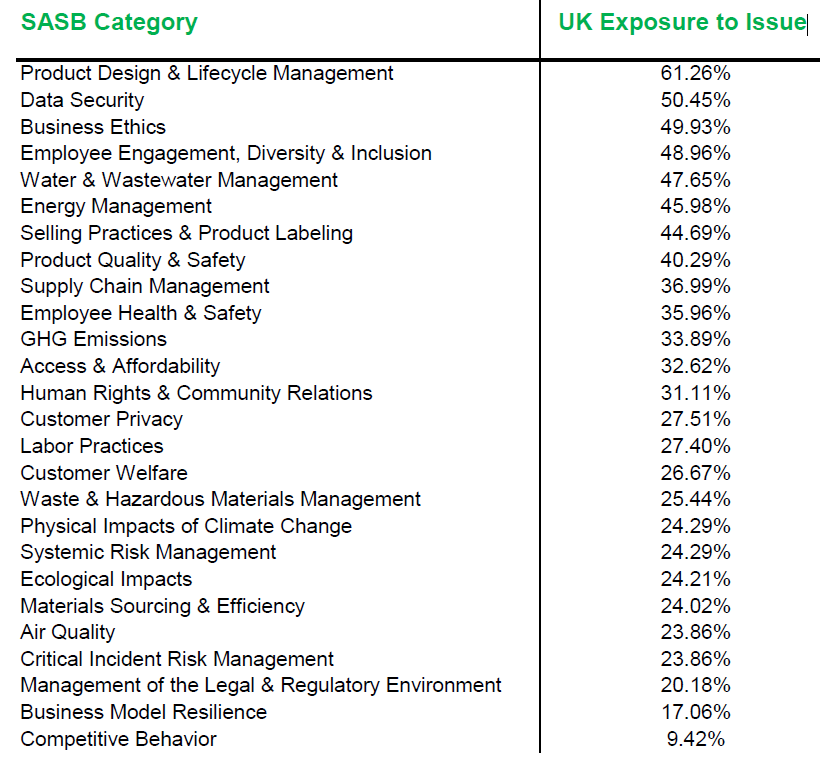

Looking one level deeper, the largest dimension exposure is in Social Capital, but the sustainability issue the UK market has most exposure to is Product Design & Lifecycle Management, which falls under the Business Model and & Innovation Dimension. This addresses the incorporation of ESG considerations in characteristics of products and services, encompassing lifecycle impacts (i.e. packaging and distribution) and other environmental and social externalities that may occur. Notably, the issue captures companies’ ability to address customer and societal demands for more sustainable products and meet evolving environmental and social regulations.

Materiality Exposure of FTSE All-Share ex Investment Trusts

| Dimension | UK Exposure to Dimension |

| Environment | 59.79% |

| Social Capital | 96.02% |

| Human Capital | 82.85% |

| Business Model & Innovation | 90.65% |

| Leadership & Governance | 67.39% |

Product Design & Lifecycle Management is a material issue for over 60% of the FTSE All-Share, followed by Data Security and Business Ethics which perhaps isn’t surprising given shifting focuses in consumer demand to sustainable products and regulatory developments across data security and worker treatment. The anticipation of these material risks is already feeding through to corporate philosophy, future planning and target setting. Company to company the focus will vary, but the use of recyclable materials, net-zero carbon targeting, and diversity & inclusion goals are examples of addressing these matters. The issue of least materiality at under 10% exposure is Competitive Behaviour suggesting that the UK equity market’s least area of concern (relatively) with regards to impact on future cashflows, are anti-competitive practices such as collusion, price-fixing and the existence of monopolies.

Frameworks such as materiality maps aren’t perfect, and the process of determining which issues are material to which companies can be highly fact-specific and labour-intensive. Subjectivity is inherent, along with numerous metrics and methodologies and the detail really matters. But they can help individual investors in developing their own view on what is most material. Applying the SASB framework and backing out the largest material issues can yield interesting results at an index level. In the UK equity market’s case, or the FTSE All-Share to be precise, given the times we live in, the importance of social capital cannot be understated.