Several recent studies have highlighted how fixed income strategies that integrate ESG factors into their investment process have outperformed the wider market during the ongoing Covid-19 crisis.

Our analysis also confirms this, but we don’t think the observations made during the unprecedented circumstances of this year should be the sole driver of institutional long term fixed income allocations. Assessing the data across a longer period of time should enable investors to make more informed decisions.

When analysing data from 2007 to June 2020, we observed that, in most cases, ESG integration into fixed income portfolios didn’t, at the very least, impact performance negatively. This period is relevant because it coincides with the global financial crisis and strong implementation of unconventional monetary policies, which after an eventual pause, resumed again with the Covid-19 crisis.

See also: – Can ESG outperformance continue?

More precisely, we backtested the performance of monthly rebalanced long-short (L-S) portfolios to find out the effects of overweighing (under weighting) higher (lower) rated ESG bonds. We did this for corporate and sovereign bonds for both developed and emerging markets, and for different chosen segments (selected country groups for sovereign bonds, ratings and sectors in the case of corporate bonds).

Positive results for EM sovereign bonds

In the case of sovereign bonds, the construction of portfolios which went long for the highest-ESG rated bonds and short for the lowest ESG-rated bonds in emerging markets delivered significantly better risk-adjusted returns. In particular, it may have been a mitigating risk factor in portfolios performance during the recent Covid-19-related sharp market decline.

Incorporating the social and governance factors yielded significant positive results while the integration of environmental issues in sovereign bond portfolios did not lead to significant performance results. Clearly this result is hardly surprising given that sovereign credit risk has traditionally been assessed through variables that characterises political, social and economic risk. Key factors such as governance and its effectiveness, corruption, political instability, education, inflation, fiscal policy, GDP growth, etc. have always been scrutinised by credit agencies, markets and academics. On the other hand, the Environmental risk factors analysed by ESG providers have not been used that much historically by credit agencies and markets for assessing sovereign credit risk.

In developed markets the results were a lot less significant. However, we believe that these results are likely to change in the future, particularly with the growing importance of environmental factors and the international treaties being signed to fight against climate change. Governments are likely to be increasingly scrutinised by agencies and markets in this context.

Positive results for developed markets corporates

Investment grade corporate bond performance in L-S portfolios highlighted that, overall, the integration of ESG was effective for issuers in developed markets – but not as significant in emerging / frontier markets. Overweighting corporate bonds with better ESG quality in developed corporate markets delivered positive risk-adjusted returns in various market segments – especially for the BBB segment in industrials and utilities – with the environmental factor acting as a key differentiator, particularly from 2012 onwards – when MSCI extended its ESG rating coverage – followed by social and governance, in that order.

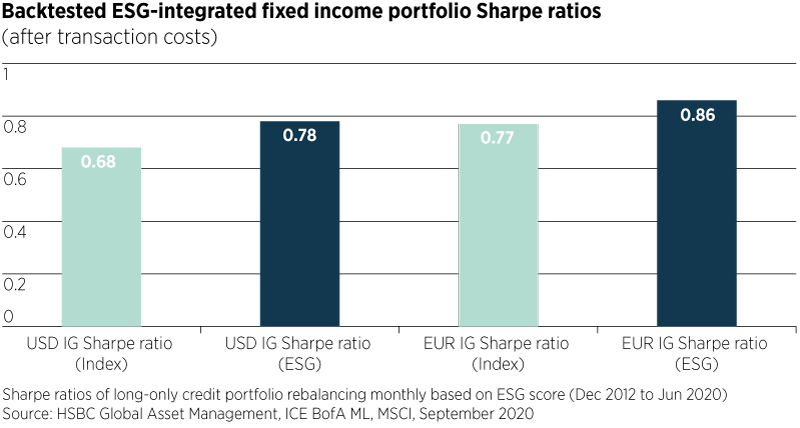

When testing ESG signals in long-only investment grade corporate bond strategies in developed markets, the portfolios delivered positive risk-adjusted returns for EUR and GBP issuers before transaction costs. The outperformance after transaction costs remained positive, though with lower information ratios.

The ESG factor

Given that ESG scores have not been in use for very long, we can’t say that an ‘ESG factor’ has been identified. In other words, we can’t say that integrating ESG considerations into a fixed income portfolio would systematically improve its performance. However, what’s clear is that the integration of ESG in fixed income portfolios did not harm returns. In fact, during the period of time analysed, it added value to investors in most circumstances.

Nevertheless, it is important to note that, according to our research work, ESG high-rated bonds tend to have a lower beta. They generally allow a clear reduction of risks but may also imply – and to a minor extent – a potential reduction of the absolute performance. It means that the integration of ESG in a fixed-income investment solution requires an informed and sensible portfolio design in order to mitigate unwanted bias.