Investment industry groups have welcomed the UK Financial Conduct Authority’s (FCA) Sustainability Disclosure Requirements as a “marked improvement on the EU’s SFDR” as the chance to respond to the regulator’s proposals closes this week.

“We are very pleased to respond today to the FCA’s consultation on sustainability disclosures and investment labels,” said James Alexander, CEO of the UK Sustainable Investment and Finance Association (UKSIF) and ESG Clarity EU Committee member.

“We agree with the FCA’s characterisation set out of what constitutes a sustainable investment, which represents a marked improvement on the EU’s SFDR.”

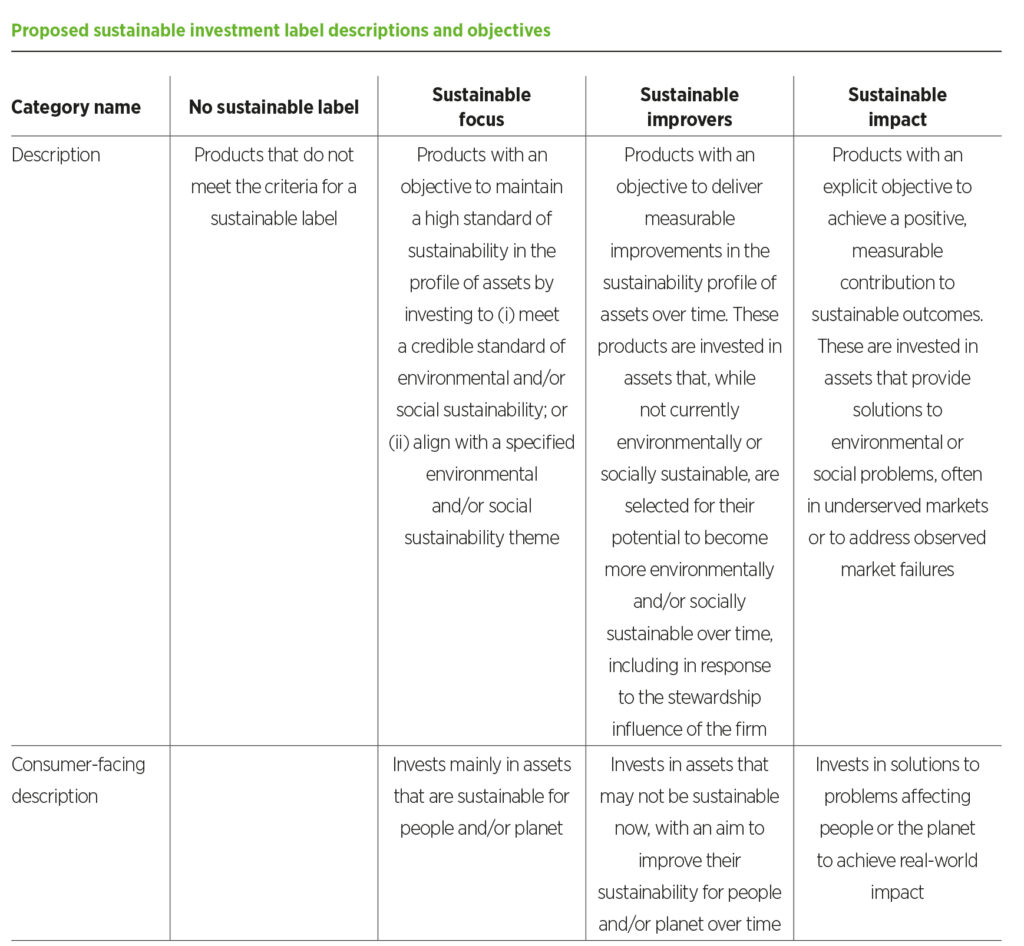

The FCA’s consultation paper, which published in October last year, set out three investment labels for sustainable funds: “sustainable focus” funds that invest in sustainable assets, “sustainable improver” funds that invest in assets looking to improve their sustainability over time, and “sustainable impact” funds that invest in solutions.

UKSIF was joined by Morningstar and the Institutional Investors Group on Climate Change (IIGCC) in praising the labelling decisions in their responses to the consultation.

“Restricting the number of labels to three and confining them to those products that commit to the strongest ESG aims within their objectives, strategy and measurement should result in only the most committed products electing a label,” Morningstar’s response read.

“That said, we anticipate very few retail investment products will be able to satisfy the proposed requirements for an impact label due to associated liquidity and portfolio concentration regulatory constraints.”

The IIGCC also flagged some concerns over the labelling, namely that the three appear mutually exclusive. “Many investors pursuing sustainable objectives, including alignment of their portfolios with net zero, and across a range of asset classes, will in practice adopt a blended strategy for achieving this,” it said.

The consultation asked respondents about each label individually:

Sustainable focus

Responders differed over this category’s threshold of containing 70% sustainable investments. While UKSIF and the IIGCC welcomed it – with the latter saying it will likely need to “ratchet up over time to support the UK’s climate targets” – Morningstar said it was likely “to be a high bar for many based, based upon our analysis of SFDR Article 8 and 9 funds”.

The groups also saw potential pitfalls in how the label is implemented and how it may apply differently across asset classes. The IIGCC also asked for clarification on the remaining 30% of holdings, which is said “without appropriate guardrails, could create a risk of greenwashing”.

Sustainable improvers

Stewardship is clearly a vital component for funds seeking this label, which the respondents welcomed, although UKSIF noted this could be a category open to a very large number of funds.

UKSIF was also concerned with how the actual ‘improvement’ of a fund’s holdings might be measured and reported. “In the short term, we see the lack of consistent, clear guidance and metrics outlined in order to measure the performance and characteristics of funds in this category, specifically the extent to which they are ‘improving’ and transitioning, as a real issue,” it said.

Morningstar agreed evidencing the effectiveness of engagement practices “will be difficult to assess based on fund disclosure” and therefore proposed the criteria should include disclosure of voting records on ESG resolutions (e.g., % voted ‘for’, ‘abstain’, ‘against’ in the last cycle) as a way to hold these funds clearly accountable for this dimension of the stewardship work.

Sustainable impact

UKSIF and the IIGCC agree ‘impact’ is the appropriate term for this category of funds, for which additionality is a key feature, with the latter recommending the FCA considers aligning its definition of impact investing more closely with that established by the Global Impact Investing Network “in the interest of international consistency and best practice”.

However, Morningstar had another suggestion.

“All three labels are about creating impact but in different ways. Using the term ‘impact’ for one label suggest that the other funds are about something else or create less impact,” the firm said.

“For these reasons we suggest there is a case for calling this label ‘Sustainable Solutions’ or something similar. Such a change could also soften the assumption that this label is not inclusive of investment in public equities.”

Next steps

Once the nuances of the labels are ironed out, the practicalities and enforcement of them will come into question.

“Given the inconsistency in the quality of some sustainability data, we encourage the FCA to consider requiring external verification of labels” said Edina Molnar, vice-president in Redington’s investment consulting team.

“This would allow for greater accountability and stronger consumer trust. We also encourage the FCA to provide clarification around how the labelling and disclosures requirements will be enforced, including details on the consequences of breaching the regulations.”

Overall, however, the direction of travel for the FCA’s proposals appears positive.

Alexander concluded: “We remain optimistic the upcoming regime will contribute to rebuilding trust among savers in the sustainable investment choices available to them, and delivering the ‘high bar’ for funds seeking to make sustainability claims.”