The introduction of the Sustainable Finance Disclosure Regulation (SFDR) is seen as one of the key milestones for the accomplishment of the EU action plan for financing sustainable growth.

Even as the technical standards for the full implementation of this regulation are not in place yet, it is worthwhile to analyse how fund promoters and investors act with regard to fund launches and investments under the new SFDR classifications according to the articles 6, 8, and 9.

While the former can be measured by the number of funds (primary share classes) classified as article 6, 8, or 9 compliant, while the latter can be measured by the estimated net flows in each of the categories.

To analyse if and how the SFDR regulation has been adopted by fund promoters and investors, we will shed a light on those funds which have been launched in a European domicile between 1 January 2021, and 30 September 2021.

Fund launches

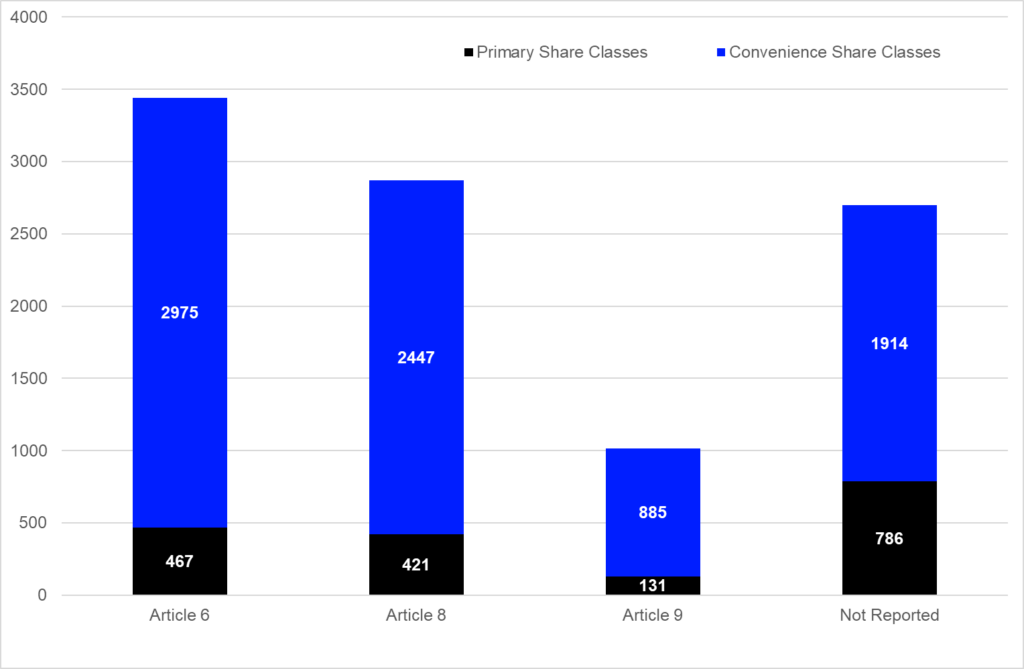

According to the Refinitiv Lipper database, there were 10,026 newly launched funds in Europe over the course first nine months of 2021. 1,805 of these products were primary share classes, while 8,221 were so-called convenience share classes. Even as the fund flow analysis will examine the flows for all share classes, the main focus for fund launches is on the primary share classes, as these represent the number of newly launched portfolios.

Number of fund launches in Europe (01.01. – 30.09.2021)

As equity funds are the largest asset type in the European fund industry, it is not surprising that equity funds witnessed the highest number of primary fund launches (781) over the course of the first nine months of 2021. Mixed-assets funds witnessed the launch of 507 new primary share classes, followed by bond funds (327), alternative UCITS funds (88), “other” (43), money market products (32), commodities funds (14), and real estate funds (13).

Surprisingly, the highest number of fund launches for all asset types (786) can be found in the category not reported. Given the fact that the industry is still lacking the technical standards for the implementation of the regulation, this might be an objective of change.

Nevertheless, the majority of newly launched funds is classified under one of the three articles (1,019). Within this group the highest number of funds is classified under article 6 (467), followed by funds classified under article 8 (421), and article 9 (131).

Contrary to the public discussions by market observers, these numbers show that the fund industry is still launching more conventional, rather than ESG-related, products. Therefore, it is worthwhile to analyse the categories that are preferred by investors.

Fund flows

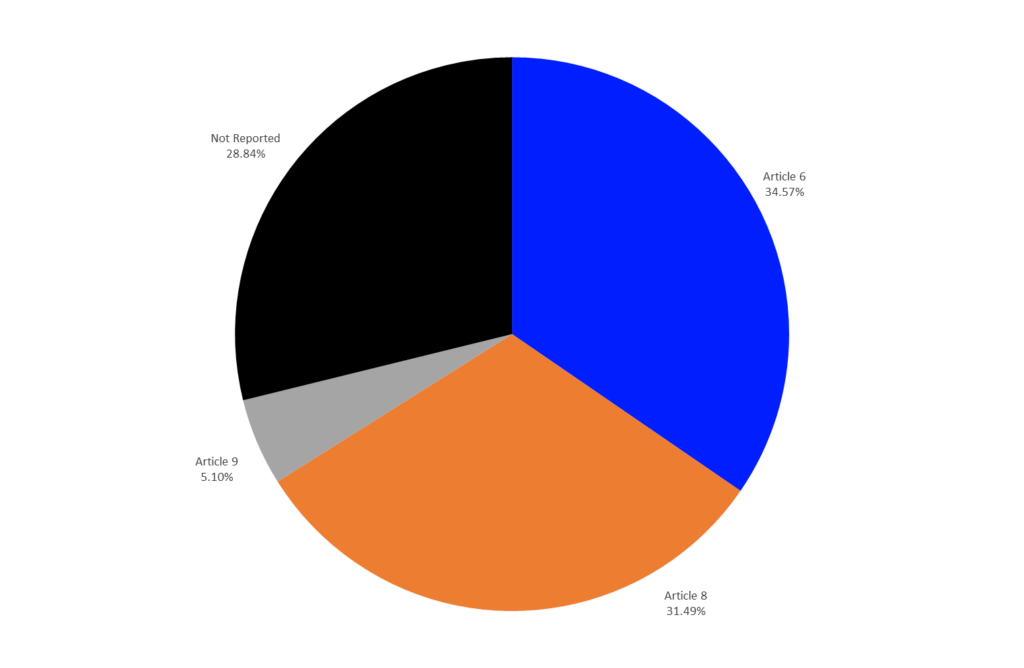

European investors invested a total of €184.9 bn in funds and ETFs that were launched after December 31, 2020. Mutual funds and ETFs categorized as article 6-compliant enjoyed the highest inflows (+€63.9bn), followed by article 8-compliant products (+€58.2bn), products that have not reported their status (+€53.3bn), and article 9-compliant mutual funds and ETFs (+€9.4bn).

Market share of fund flows by SFDR Classification (01.01. – 30.09.2021)

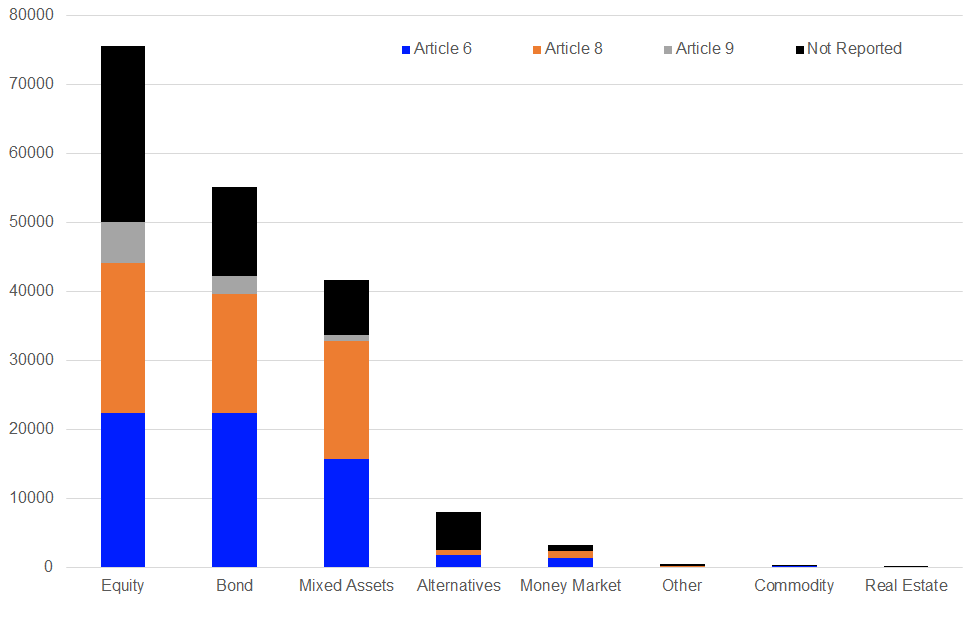

In more detail, equity products enjoyed the highest inflows (+€75.6bn), followed by bond products (+€55.2bn), mixed-assets products (+€41.7bn), alternative UCITS products (+€8.1bn), money market products (+€3.2bn), “other” products (+€500m), commodities products (+€400m), and real estate products (+€100m).

Given the current discussions around sustainability in general and sustainable investing in particular, it is somewhat surprising that newly launched funds which have not reported their SFDR status yet enjoyed the highest inflows (+€25.5bn) in the equity segment. With regard to this, it is noteworthy that funds which are domiciled outside the EU have no obligation to report their SFDR status as long as they are not distributed in the EU.

Fund flows by asset type and SFDR classification year to date (in bn EUR)

Funds which are compliant with article 6 enjoyed the highest inflows (+€22.3bn) in the bond (+€22.3bn) and money market (+€1.4bn) segment, while funds compliant with article eight (+€17.2bn) were leading the fund flows table for mixed-assets funds. With regard to the market exposure of the asset classes, it was no surprise that the highest inflows for alternative UCITS funds (+€5.5bn), “other” funds (+€300m), commodities products (+€200m), and real estate funds (+€100m) occurred in products that have not reported their status so far.

These figures show that investors prefer newly launched funds with lower ESG standards. This could also be in the interest of fund promoters, as non-ESG funds require less effort from a fund management perspective, since they do not have to integrate ESG data into the asset management processes of the respective funds and can therefore have lower operating costs.