Asia may play an outsized role in global GDP growth, but it is viewed as a laggard when it comes to addressing environmental, social and governance (ESG) issues. Air pollution in China is famously chronic. Inequality in India in deeply entrenched. Nepotism and corruption in parts of South East Asia is rife. The list seems endless.

On the surface, Asia scores poorly on key ESG issues, admits Matthews Asia portfolio manager Vivek Tanneeru but, he adds, the region is changing fast.

“ESG is an area of growing importance in the region and stands to become an important theme in Asia in the future,” says Tanneeru, who co-runs Matthews Asia $20.9m ESG fund. “Many countries in Asia are making strides toward clean energy innovation, supported by positive regulatory trends.”

After ignoring China’s crippling environmental problems for years, for example, the Beijing government is now tackling them head on. “Chinese policy makers are now prioritising pollution issues,” says John Lin, China portfolio manager, at Alliance Berstein.

This shift in focus comes at a time when the United States, under President Donald Trump, has put environmental concerns on the backburner and has withdrawn from the Paris climate accord.

Solar and electric cars

The impact that solar energy could have on the global economy is almost limitless. Solar technologies such as photovoltaics, solar hot water and concentrated solar power could provide a third of the world’s energy by 2060, according to the International Energy Agency.

China is at the forefront of this shift: it now makes about 70% of the world’s solar panels and installs more than half of them.

“China is becoming a world leader in areas such as renewable energy and sustainable transportation infrastructure,” Tanneeru adds.

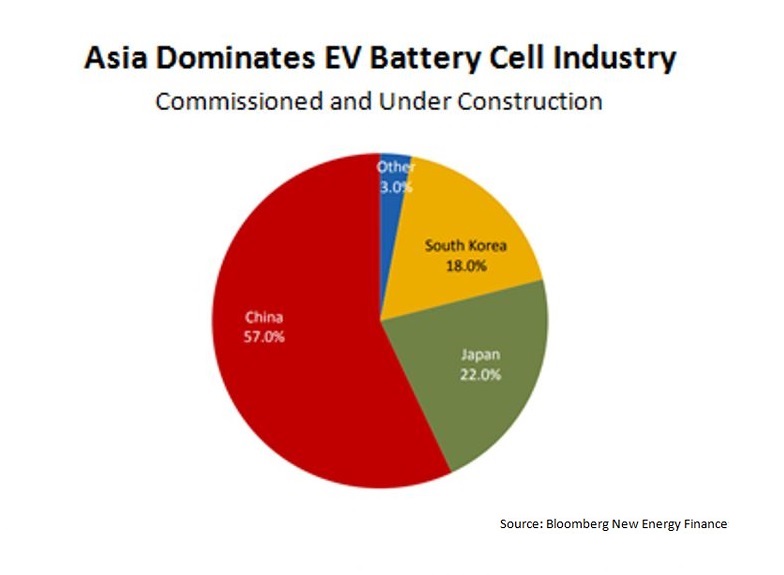

Tesla’s stylish Model 3, meanwhile, may have become the poster child for the electric car revolution. But beneath the bonnet many prototypes rely in rechargeable batteries made in Asia. The top lithium-ion battery makers in the world are in South Korea, Japan and China.

Asia has historically dominated the manufacture of consumer electronics, which often require rechargeable batteries, and this legacy has given Asian manufacturers an edge.

Indeed, Asia also accounts for a significant portion of new electric vehicle sales. China is the world’s largest market for electric vehicles (the US is a close second).

Of the two million electric cars on the road in 2016, 32% were driven in China, while 28% were driven in the US; Japan and France each represent 7%.

A growing middle class

Inclusion ranks near the top of social issues that Asian countries have to grapple with. Social advancement begins with moving hundreds of millions of people out of poverty. It requires bringing more people into the middle class; greater access to health care; more women in the workforce; and more opportunities for people to advance through education and training.

“These shifts present a prime opportunity for global investors who wish to support this progress by investing in companies championing inclusion in Asia’s fast-growing economies,” Tanneeru said.

Millions of people across Asia lack basic banking services. Therefore, a first vital step towards a middle-class life is access to the formal financial system and the ability to open a bank account.

Credit, even in small amounts, can make a huge difference to families living in poverty. And across Asia, microlenders are leveraging digital platforms to scale up lending without the need to build large brick-and-mortar infrastructure.

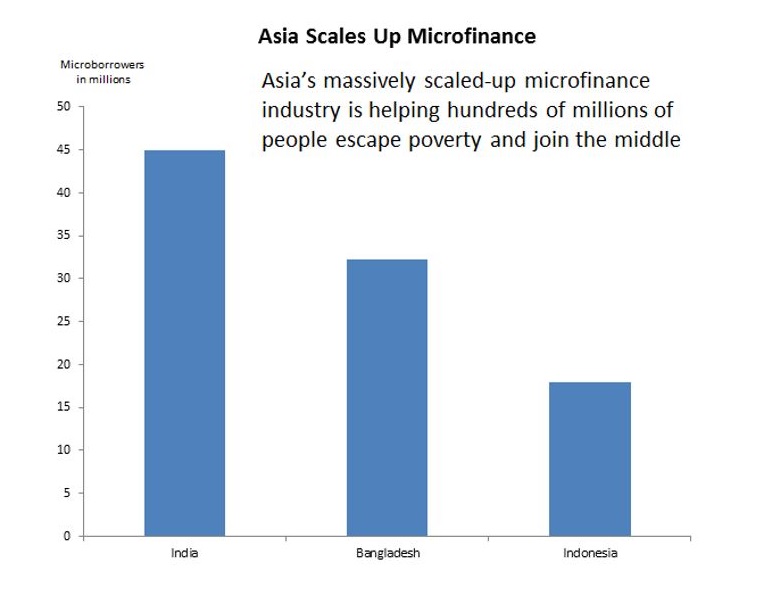

Profitable companies servicing this need provide microlending, micropayments and insurance. In 2017, India had 45 million microborrowers, demonstrating the size and scale of this growing marketplace.

Bangladesh and Indonesia are also fast-growing markets for micro and small enterprise lending.

“Micro and small enterprise lending is an underappreciated social opportunity.” Tanneeru argues.

“Most jobs in emerging Asia are found in micro and small enterprises. Access to capital financing, therefore, could make an enormous difference in the ability of these firms to grow and create more jobs.”

Healthcare costs

At present, Asian countries have some of the lowest per-capita spending on healthcare in the world. Driving down the cost of healthcare is obviously a crucial step towards greater social progress in Asia – fulfilling another key ESG criteria.

Tanneeru argues that a number of indicators suggest the region is at a tipping point.

South Korea, for example, has become a leader in the manufacture of biosimilars –biopharmaceutical drugs designed to have active properties similar to those that previously been licensed but at a more affordable price.

“They are likely to tap a big market in Asia where health care needs and spending are rising,” Tanneeru said.

China, meanwhile, is emerging as a novel biologic drug innovation hub and India has fostered one of the world’s largest manufacturers of generic drugs.

Governance progress

Key components of robust and transparent financial markets are trust and accountability.

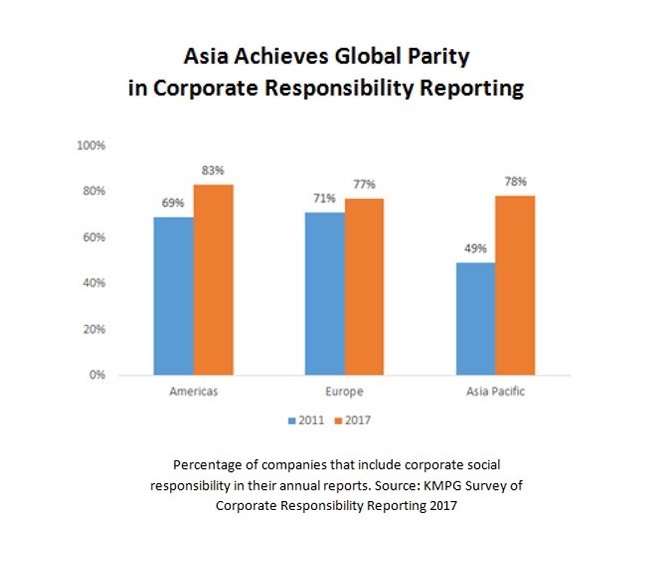

“Asia has made tremendous progress over the past six years increasing transparency,” Tanneeru argues, adding that it had achieved “parity” with Europe and North America in corporate responsibility reporting.

In 2011, just 49% of large Asian companies reported on corporate responsibility, but that number rose to 78% by 2017 – comparing favourably to 77% of European companies and 83% of the Americas.

There is still, of course, much to be done. Many gaps still exist in reporting on broader ESG issues, especially when it comes to small and mid-sized companies, as well as companies in less-developed parts of Asia.

Matthews Asia ESG fund is invested in South Korean tech giant Samsung, for example, which has been beset by corruption scandals and allegations that management has sabotaged labour union activities.

And even among the more technologically advanced Asian countries, gender diversity is woefully behind the west. Women sit on only 4.2% of corporate boards in Japan. In South Korea, the figure is just 2.5%.

But the growth potential remains enormous and, as Tanneeru repeats, Asia is changing fast.

“New growth industries, such as battery cells for electric vehicles and microlending platforms, must be evaluated through fundamental metrics including cash flow and balance sheet analysis to determine which businesses are likely to generate solid long-term revenue growth and sustainable profits.”

“Integrating ESG data into the investment process can help investors capture this growth potential through a disciplined, long-term approach to investing,” he says.

– This article first appeared on ESG Clarity‘s sister site Expert Investor.