Morningstar has removed the sustainable investment label from more than 1,200 European-domiciled funds over the last few months, as the firm said more funds are likely to be reclassified in the coming weeks.

In its fourth quarter review of global sustainable fund flows, the group noted it had made an “extensive review” of fund documents in Europe. The result was reverting to its pre-SFDR (Sustainable Finance Disclosure Regulation) European universe of sustainable funds.

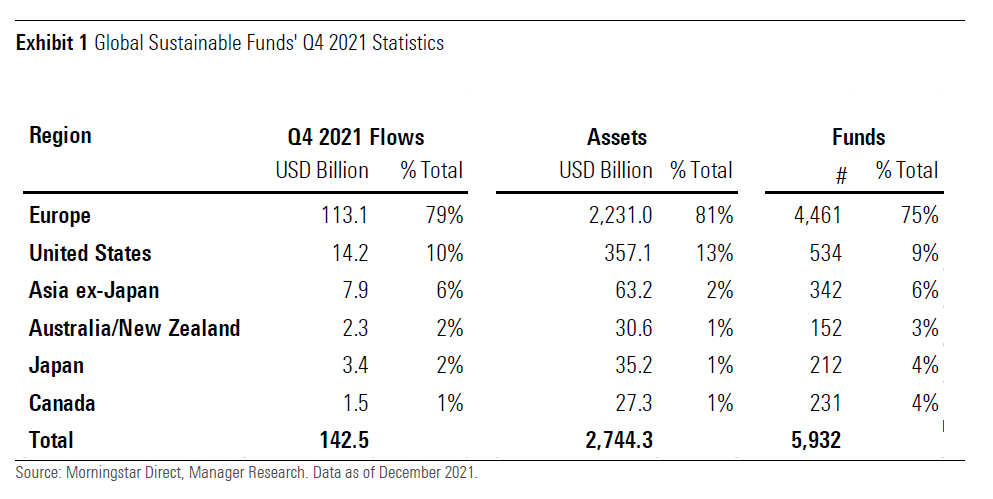

Although the universe includes newly launched or repurposed funds which meet Morningstar’s sustainable fund criteria, it is still 27% smaller than in the third quarter of 2021 – at 4,461 funds.

Pain in the SFDRs

The group’s review on sustainable funds from the third quarter stated there had been a 78% growth in the European fund universe from 3,444 at the end of March 2021 to 6,147 at the end of September. Morningstar cited this growth was thanks to new ESG disclosures in fund documents following the introduction of SFDR in March last year.

“In recent months, however, Morningstar data analysts have revisited these disclosures and tightened their criteria to tag funds as sustainable investments in the database,” the review stated.

Many of the culled funds were self-classifying as promoting environmental or social characteristics under Article 8, more of which will be “untagged” in the coming weeks, Morningstar added.

Elsewhere, the report explained why Morningstar was tightening sustainable investment criteria: “Identifying the European sustainable funds universe has always been a challenge, but it has become even greater since the introduction of the SFDR on 10 March 2021.

“SFDR, which aims to increase transparency on the ESG risks and impact characteristics of investment products distributed in the European Union, has substantially increased the volume of ESG-related disclosures in legal documents, as intended.

“However, it has also led to confusion and suspicion of greenwashing. Many funds that place themselves into Article 8, for example, are not funds we would independently classify as sustainable funds.”

A Morningstar spokesperson said: “Since the publishing [Global Sustainable Fund Flows: Q3 2021 in Review], Morningstar has modified over 1,200 funds from being a sustainable investment due to additional documentation (prospectus, annual report, etc) and developing further best practices and guidelines noting how companies differentiate their sustainability-focused range.

“Morningstar continues to strive to improve its processes to identify sustainable investments as market standards and available data evolve.”

Majority of flows sustainable

The report stated flows in to sustainable funds made up 58% of overall flows in European funds in the fourth quarter of 2021. There were $113.1bn in net inflows to sustainable versus $82.2bn for conventional funds.

Sustainable fund flows increased in Europe by 20% in the fourth quarter of the year compared to the third. In the same period conventional fund flows decreased by 32%.

This was mirrored in the global picture where the sustainable flows increased 12% from the previous quarter, up to $142.5bn, while overall the global fund universe saw a 6% drop in flows.

Europe accounted for 79% of the global sustainable flows in the last quarter of 2021.

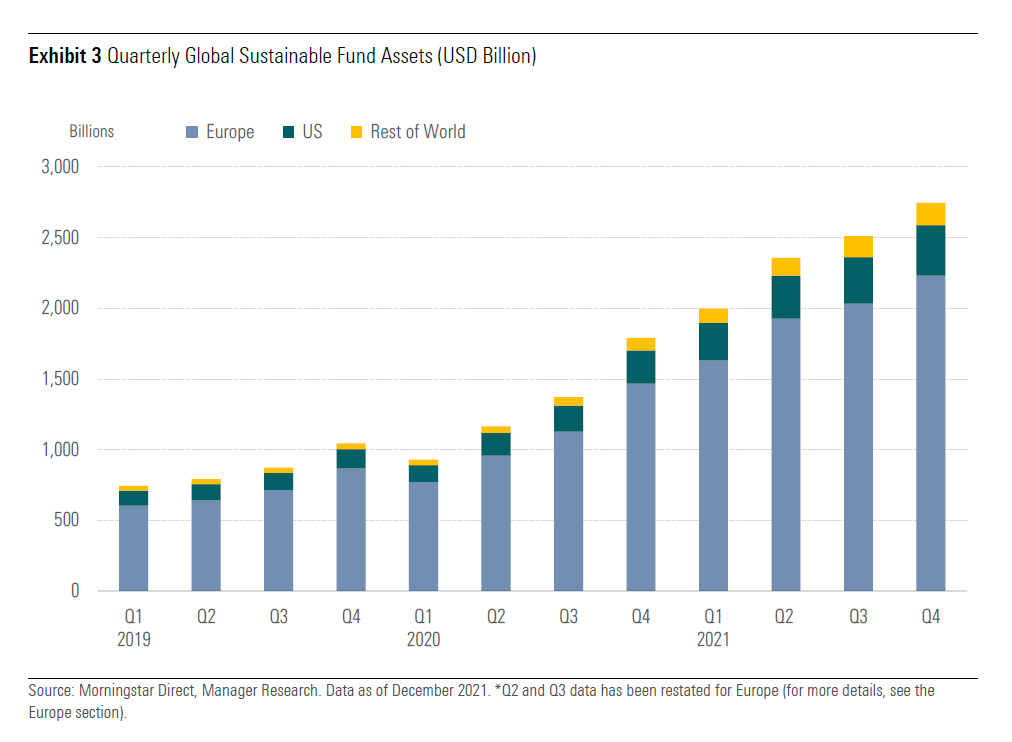

Overall, the sustainable fund universe grew to $2.74trn to the end of last year.

Repurposed funds double

Morningstar identified 536 funds repurposed as sustainable in 2021, roughly double the figure for 2020.

The group described the regulatory environment in which the increase took place: “This all-time high was reached as asset managers seized the opportunity of having to publish new SFDR-compliant prospectuses to review their offerings, add binding ESG criteria and exclusions, and, in many cases, rebrand their funds.

“Transforming existing funds into sustainable strategies is a way for asset managers to leverage existing assets to build their sustainable-funds business, thereby avoiding having to create funds from scratch.

“This may also be a way for fund companies to reinvigorate ailing funds that are struggling to attract new flows. Others may choose to ‘green’ their entire range of funds by, for example, expanding their exclusion policies and divesting from the biggest carbon emitters.”