Classifying funds as Article 8 or 9 under the EU’s Sustainable Finance Disclosure Regulations (SFDR) could mean larger inflows, but investors have been warned assessing the degree of genuine ESG integration for these strategies is difficult.

London-based ESG advisory and analytics firm MainStreet Partners worked with White Marble to analyse the ESG fund and ETF landscape almost a year on from the introduction of SFDR in order provide their clients with an “unbiased understanding” of the evolving industry.

Looking at MainStreet’s universe, which consists of 4,200 funds and ETFs run by 160 asset managers and amounting to €5.6trn in AUM, only 5% were classified as Article 9 – funds considered to have highest integration of sustainable characteristics (see table below).

SFDR definitions

The research, detailed in its ESG Barometer, report Some 25% of the universe was classified as Article 8, while most funds (70%) were under Article 6.

However, the report warned investors against taking these labels at face value.

“Overall, the classification of funds under Article 8 and 9 has correlated with larger inflows into these products suggesting that investors are placing their trust in the labels. However, assessing the degree of genuine ESG integration has arguably become more difficult, given the diversity of products on show and the absence of standardisation.

“Around a fifth (21%) of funds that have been classified as Article 8 have achieved a MainStreet Partners ESG fund rating of less than 3 out of 5, missing the threshold of 3, meaning that they would not be classified as ‘sustainable’ by MainStreet Partners.”

Additionally, MainStreet found commonality in terms of ESG risk ratings when looking at Article 6 and 8 funds, and in some cases Article 6 funds scoring higher than Article 8 counterparts, indicating asset managers have different interpretations of the categories.

“This is likely in part due to managers who in exercising caution chose to initially classify all their products as Article 6, and we anticipate that those funds with an ESG score of more than 3 will be transitioned to Article 8 in the early part of [this year]. Managers who chose to initially classify all their offerings as Article 8 will also be contributing to the high level of variation within that category.”

It added some asset managers have been concerned about classifying their funds in too high a category, and others have listed the majority of their funds as Article 8. Noticeably, US-headquartered asset managers have transitioned more funds, whereas European and UK groups are “adopting a wait-and-see approach”.

The report concluded in this area there is further work for the regulators.

“Further clarification is necessary from the regulators, especially with regards to Article 8 funds. There is such a wide variety of them; from those employing basic exclusionary criteria, to those with additional layers of ESG integration and reporting, through to thematic ESG funds. Indeed, we have even seen the adoption of a qualitative informal classification of so-called ‘Article 8 plus’ funds by asset managers, attempting to bridge the gap between Article 8 and 9. This further classification results from the Mifid II draft sustainability assessment, which can be considered more stringent than SFDR, as it combines the Taxonomy Regulation and SFDR regulation to encompass clear sustainability preferences of invested financial instruments.”

Asset managers

Reflecting research from Morningstar in the first 10 days of SFDR last year, Amundi and BNP Paribas had the highest number of Article 8 and 9 funds followed by Eurizon, JP Morgan and BlackRock. Interestingly, Candriam had a significant number of Article 9 funds but had a lower amount of funds categorised in total.

The report also surmised size does not matter, with boutiques having higher ratings in terms of ESG strategy and portfolio level. This is down to boutiques presenting more innovative strategies, having strong monitoring and reporting processes as well as investing in securities with higher ESG ratings and less controversies, according to the report.

“Some sustainable boutiques’ portfolios tend to show a much greater additionality, investing in differentiated securities and demonstrating higher active share,” it added.

This is despite medium and large asset managers scoring higher for ESG resources, policies and overall standing.

Asset classes

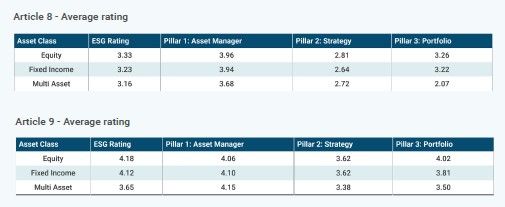

When MainStreet and White Marble looked at asset classes, they found multi-asset funds tend to have a lower degree of ESG integration and were less aligned to the UN’s Sustainable Development Goals than other categories, which the report explained being a result of “a lack of appropriate controversy monitoring procedures”.

Echoing the sentiment for investors to look beyond the labels, the report said it is “a persistent challenge” for investors to compare funds within the same category but invest in different asset classes, or those investing in the same asset class but assigned to different categories.

“For instance, all European large-cap funds may look similar if they are only analysed at the holdings level, even if the portfolio manager has made zero attempt to integrate ESG practices. Meanwhile, a fund that plays the energy transition theme specifically, or invests in small-cap companies with an impact approach, could be penalised if only the holdings are considered.”

Commenting on the report’s overall findings, Neill Blanks, research director at MainStreet Partners, said: “It is not an exaggeration to say SFDR, which came into effect on 10 March 2021, was a game changer for investors. While not yet perfect, SFDR provided a universal identification and disclosure framework for sustainability risks – something previously absent in the asset management industry.

“Overall, we have observed a high degree of correlation between the introduction of SFDR and subsequent improvement in ESG fund ratings. But while the classification of funds under Article 8 and 9 for SFDR purposes has certainly correlated with larger inflows into these products, assessing the degree of genuine ESG integration in those same funds has become more difficult due largely to the diversity of products available and the absence of a single standard for ESG-aligned products.”