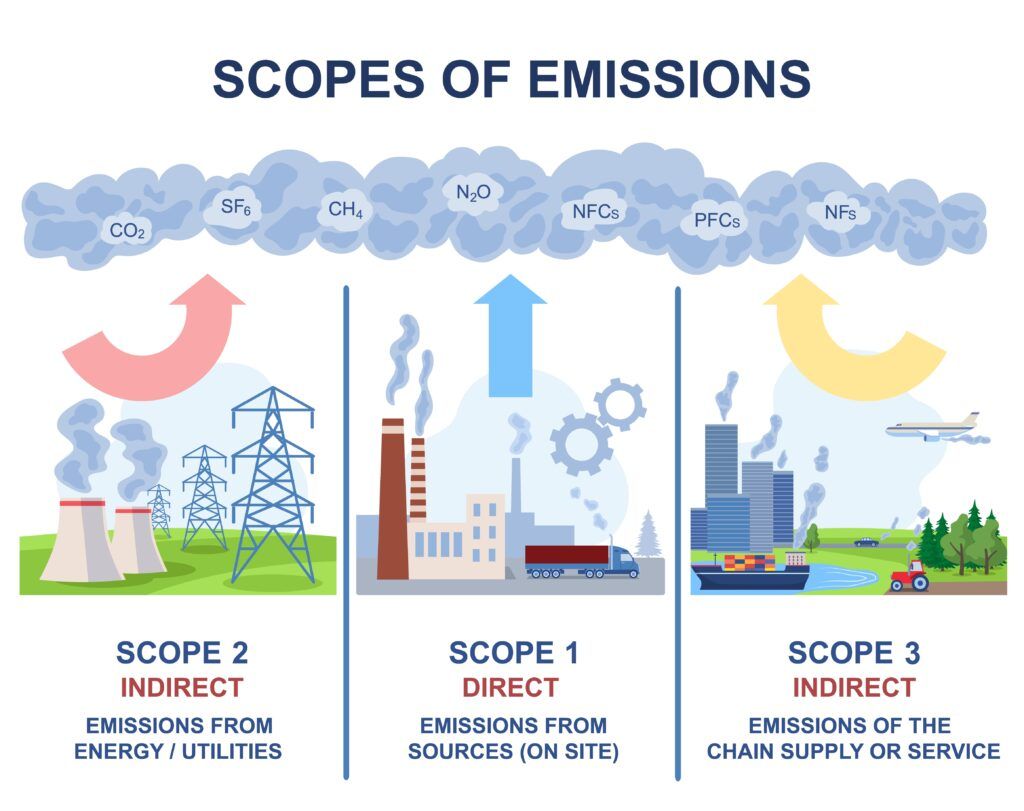

Companies will be required to disclosure on Scope 1, 2 and 3 greenhouse gas emissions, the International Sustainability Standards Board (ISSB) has unanimously decided.

Updating on its October meeting, the IFRS Foundation, which is creating the global baseline for sustainability disclosure that will be implemented early in 2023, said it had made significant progress on its draft requirements after considering feedback.

The ISSB agreed companies should disclosure on Scope 1, 2 and 3 emissions but will potentially have more time to report on Scope 3 disclosures, and also be supplied with “relief provisions” to help work out these disclosures.

This news will be welcomed by a number of asset managers that said in their feedback to the ISSB that disclosure across all three scopes is necessary for investors to obtain a complete picture of climate-related risks and opportunities, and that methodologies for disclosing Scope 3 emissions in particular will improve rapidly, according to Morningstar’s report ESG Reporting: Asset Managers Express Divergent Views.

Meanwhile, the ISSB said it has decided to modify language in the proposals that was not clearly understood, including removing the term ‘enterprise value’ from the objective and the assessment of materiality. It is also removing the term ‘significant’ to describe which sustainability risks and opportunities to disclose, and will discuss further how to refine the language it uses.

In terms of defining ‘materiality’, it will use the same definition as is used in IFRS Accounting Standards, but will look at whether further guidance is needed on how to determine what is ‘material information’.

The ISSB also confirmed the use of the Task Force on Climate-related Financial Disclosures (TCFD) architecture as the basis for its standards, and said it is working with different regulators that are working on region-specific disclosures, such as the EU, to ensure the ISSB requirements work across different jurisdictions.

Lindsey Stewart, director of stewardship investment research at Morningstar commented on the decisions: “The ISSB’s confirmation that Scope 3 greenhouse gas emissions will be required, along with Scope 1 and 2, is a positive step. To be clear, this is not a step that will please everyone given the wide range of views companies, asset managers and asset owners expressed in their feedback to the ISSB on their draft standards. And although the methods to collect and disclose information about greenhouse gas emissions are far from perfect, we don’t have the luxury of waiting for perfect data.

“Investment decision makers need this information right now to make long term decisions, so it’s important to have this certainty over which disclosures will be required so companies and investors can prepare to provide and use this information.”

Next steps

Looking ahead, the ISSB will focus on foundational work supporting the adoption and application of its first two standards – namely IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information and IFRS S2 Climate-related Disclosures.

This will include the following:

- Providing supporting materials and developing a digital taxonomy to enable digital reporting;

- Enhancing Sustainability Accounting Standards Board standards by making targeted improvements to make them more internationally applicable;

- Coordinating work with the International Accounting Standards Board to support connectivity in the two boards’ requirements;

- Researching areas for potential incremental enhancements to its proposed Climate Standard.

Giving a timeline for the next updates, a statement said: “The ISSB is carefully considering all feedback received on its proposals, while being conscious of the demand for the standards to be finalised. Its aim is to complete deliberations on the proposed standards around the end of 2022, with the view to issue the final standards as early as possible in 2023.”