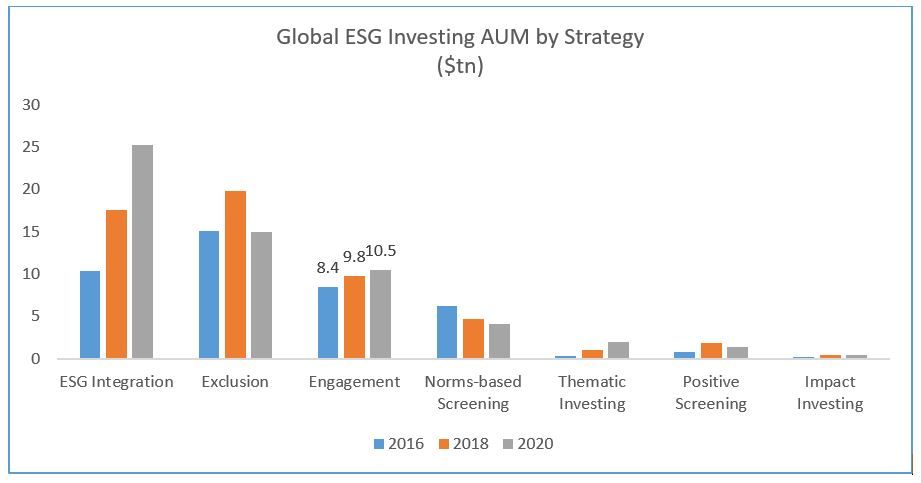

As global ESG investing continues to grow in size, strategies that incorporate engagement have swelled to the third largest ESG investment strategy after ESG integration and exclusion. Funds that employ the engagement approach manage $10.5tn in assets, up from $8.4tn in 2016.

However, although increasing recognition of the merits of such an investment strategy is important, investors must remain vigilant about emerging engagement greenwashing, or ‘engagement-washing’.

As ESG investing snowballed over the past decade, investors have been rightfully careful to navigate and sidestep investment solutions that were in name sustainability-aligned, but in practice were often rather loosely so. In response, those strategies that are genuinely sustainably-aligned have clearly articulated what full ESG integration should and must mean. With signs of similar mislabelling arising with engagement strategies, authentic engagement needs to follow the same path.

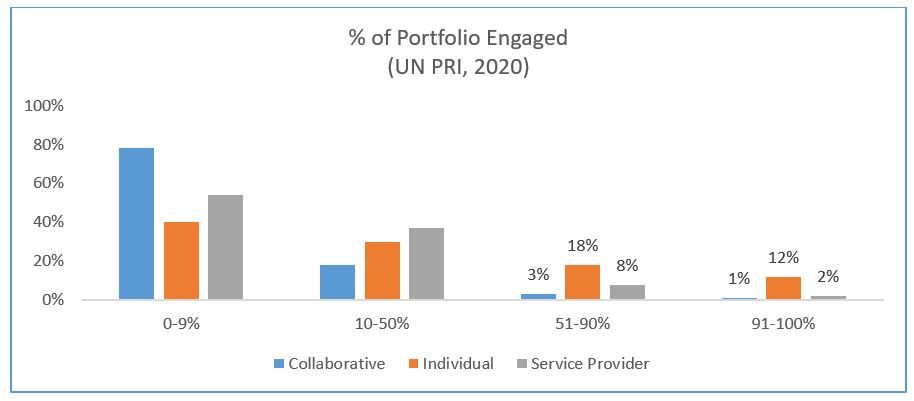

Recent studies from the ECGI and UN PRI share some interesting insights. Data was accumulated from institutional investors that spanned 1,712 engagements across 573 firms between 2005 and 2018 with assets under management in excess of $1tn. Engagement focussed on governance, strategic, environmental and social improvements. However, it seems not all engagement strategies are equal. There are four areas of potential ‘engagement-washing’ that are emerging.

First, an over-reliance on third-party service providers. Some 42% of UN PRI signatories continue to use primarily third-party service providers for their method of engagement. Second, a partial rather than a portfolio-wide approach to engagement. It appears only a fraction of investors have engaged with the majority of their portfolio companies. As of 2020, only 30% who engage individually have engaged with the majority (>50%) of their portfolio companies. Of those that engage collaboratively, this figure falls further to 18%. This is at odds to what an active engagement strategy should represent.

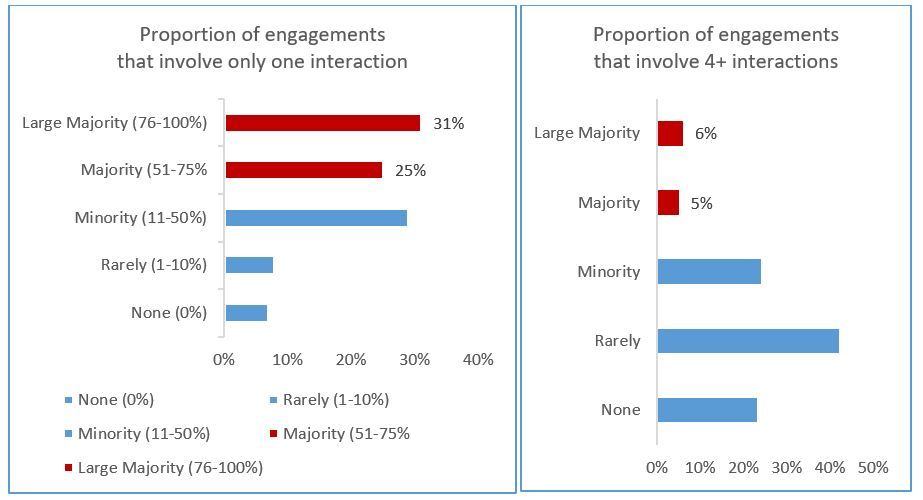

Third, insufficient depth of engagement. Some 56% of the signatories state the majority of engagements involve only one interaction while only 11% confirm that the majority of their engagements involve four or more interactions with management. As engagement takes multiple years, recurring engagements over a longer-term horizon are necessary to deliver and drive real impact.

And finally, a lack of escalation strategy. The engagement journey – despite being founded on friendly terms – can require perseverance, two-way discourse and commitment. Surprisingly, more than 60% of UN PRI signatories do not have an escalation strategy to continue to engagement with management after unsuccessful votes. This feels unsatisfactory.

Investors should be discerning. Friendly active engagement should remain the central driver of a business’s investment thesis and return profile, rather than being an afterthought once something has gone wrong. It should be deployed across the portfolio rather than on a case by case basis. Bespoke action plans should be crafted that address the most material issues to unlock hidden value and drive greater market recognition of it, rather than a singular reliance on proxy voting. This is a significantly more comprehensive and effective way to drive more impactful and long lasting change.