Despite the challenges of 2022 spilling over into 2023, demand for ESG products is expected to continue apace this year.

Energy stocks’ huge outperformance meant sustainable funds, with limited exposure, were left behind in performance tables and negative rhetoric around ESG grew in the US, making 2022 the year where the ESG world encountered more bumps in the road after two strong years.

This year is poised to present its own set of challenges with a looming recession and no signs of the anti-ESG stance taken across the pond going away.

However, ESG momentum across the asset and wealth management (AWM) industry appears to be intact, both in Europe and worldwide, according to PwC’s financial services market leader, Olivier Carré, and advisory partner, Frédéric Vonner.

They told ESG Clarity: “Although a recession and its attendant blows to traditional capital markets are expected in 2023, we expect ESG funds to outperform in terms of inflows, driven not least by growing investor awareness of the financial sector’s role in promoting sustainability-orientated transformations across industries.”

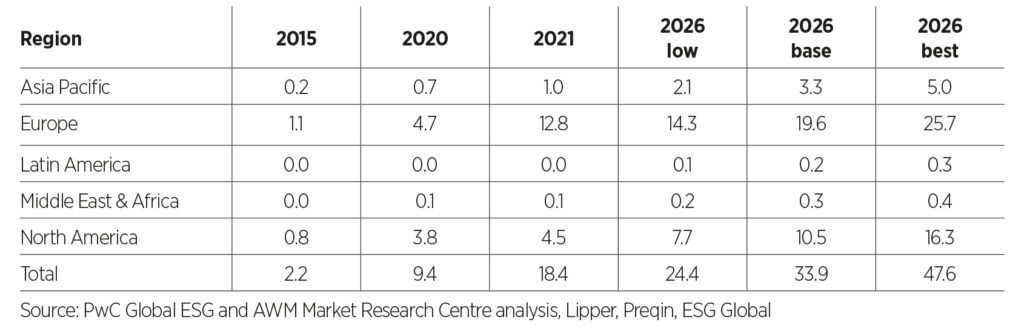

PwC data shows global ESG assets under management (AUM) stood at $18.4trn in 2032 having a compound annual growth rate (CAGR) of 42.7% since 2015. By 2026, PwC projects this number to rise to $33.9trn in a base-case scenario. Europe will lead this expansion, with its $12.8trn of ESG AUM in 2021 expected to rise to $19.6trn in 2026, at a CAGR of 12.9%.

Global ESG AUM by region ($trn)

However, they noted a number of areas that ESG product providers and users will need to be mindful of with “soon-to-be enacted rules and regulations” such as the Financial Conduct Authority’s Sustainability Disclosures Requirements (SDR) being rolled out in summer 2023.

“As disclosure requirements multiply, AWM stakeholders need to take precautions to avoid mislabelling funds and uphold investor confidence,” they warned.

Meanwhile, fund selectors have noted a number of gaps in the range of sustainable products available on the market, despite the proliferation of funds launched or repurposed in recent years.

Here, they share the products they think the market is lacking: