The outperformance of ESG funds during the covid-19 market sell-off has been extensively looked at.

Multiple reasons for the outperformance have been provided, including the typical underweighting of ESG funds to energy companies, their exposure to quality and low volatility factors, and the overall resilience of companies with high social and governance credentials. But what shouldn’t be forgotten is that ESG funds were already performing well before the crisis. Investors who would have bought an ESG fund in the past 10 years would have had good odds of success.

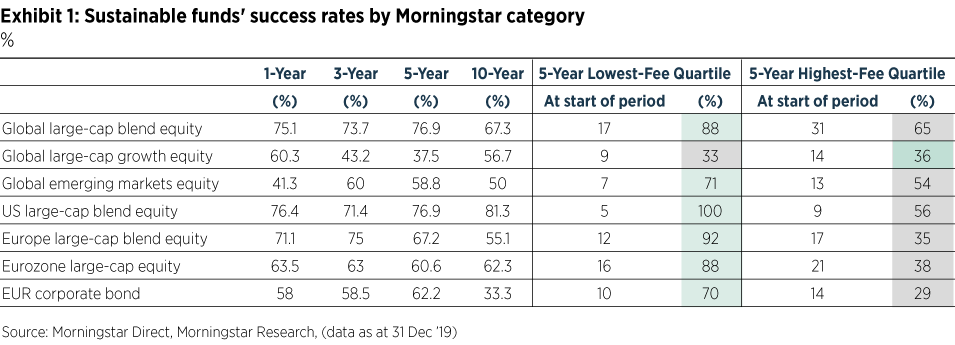

We examined the performance of sustainable funds in the seven most popular Morningstar Categories for ESG investors over the past one, three, five, and 10 years through December 2019. And we found that a majority of sustainable funds have outperformed their traditional peers over multiple time horizons (Exhibit 1).

The above-50% success rates for surviving sustainable funds in most categories over multiple time periods indicate that investors taking the ESG route were less likely to miss out on returns than if they had invested in traditional funds.

Over the 10-year period through 2019, 58.8% of surviving sustainable funds across the seven categories considered have beaten their average surviving traditional peer.

See also: – Working from Home with Morningstar’s Hortense Bioy

The odds of picking a winner were greatest in the US large-blend category. More than seven out of 10 live sustainable US large-cap equity funds delivered higher returns than their average surviving conventional counterpart. But the same can’t be said about global large-cap growth investors who would have seen their odds of success fluctuate significantly over time. Not even four sustainable global large-cap growth funds out of 10 that were selected five years ago, and are still available today, beat the average surviving traditional peer.

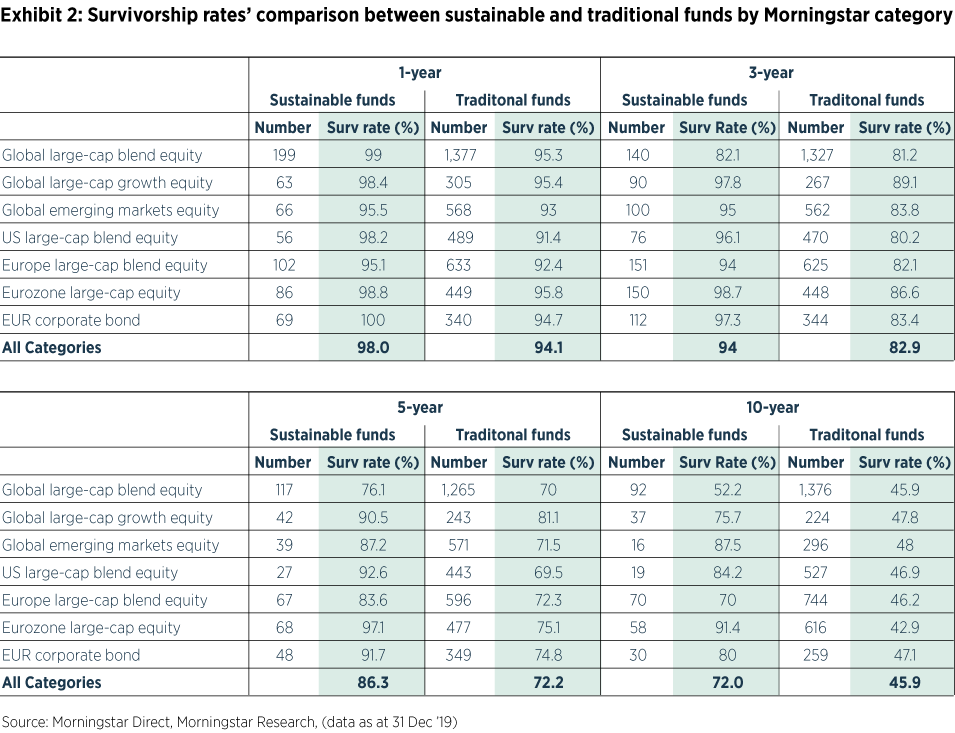

In addition, we found that sustainable funds have consistently exhibited higher survivorship rates than traditional funds over the past 10 years (Exhibit 2). This means that fewer sustainable funds have closed, in relative terms. 72% of sustainable funds available to investors 10 years ago have survived, compared with less than half (45.9%) of traditional funds.

Attrition rates were the highest in the global large-cap blend category, which also happens to be the largest category in terms of number of funds. Just 52.2% of sustainable global large-cap blend funds available 10 years ago survived. It is still better than the 45.9% odds of survival for traditional funds.

These results add to the growing body of research that show that there is no performance trade-off associated with sustainable funds. One, however, should keep in mind that the European sustainable fund universe represents a wide range of ESG approaches. It also consists of a limited number of funds with long (more than 10 years) track records, which makes any analysis of long-term performance a challenge.

Additionally, while our analysis led us to the conclusion that investors who would have bought an ESG fund in the past 10 years would have had good odds of success, it doesn’t mean that all ESG funds have had equal odds of success and that outperformance will persist. As we’ve seen, success rates have varied by market exposure and investment horizon.

Investors shouldn’t underestimate the importance of fees too. Like with any other type of investment, fees are a crucial consideration when selecting a sustainable fund. As shown in Exhibit 3, selecting a fund in the lowest-fee quartile five years ago would have improved the odds of picking a winner in all but one category. Global large-cap growth was the only category where fees didn’t give much of an advantage. Only 33% of the cheapest sustainable funds beat the cheapest traditional funds in that category.

These findings can be very valuable for performance-conscious investors looking to invest more sustainably. They can maximize their chances of success by limiting their choice to lower-cost funds.

Hortense Bioy is director of sustainability research, EMEA and APAC at Morningstar and editorial panellist for ESG Clarity. This article was based on her findings in the report How does European sustainable funds’ performance measure up?