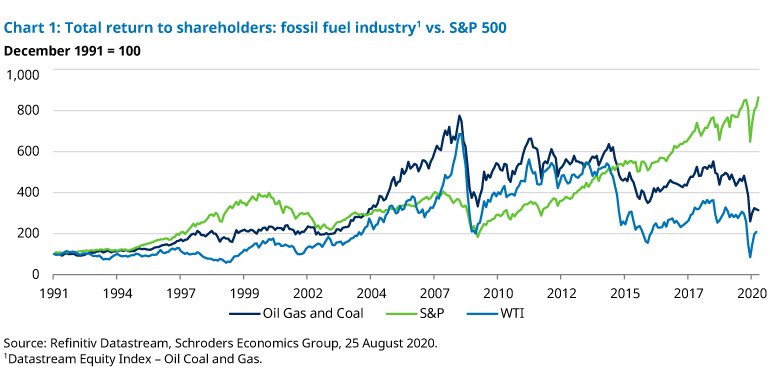

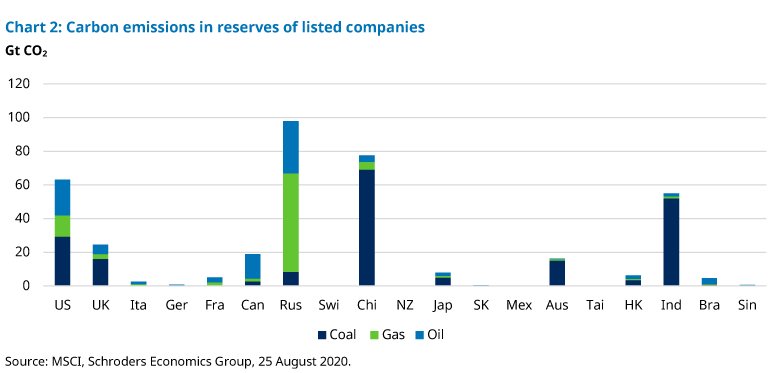

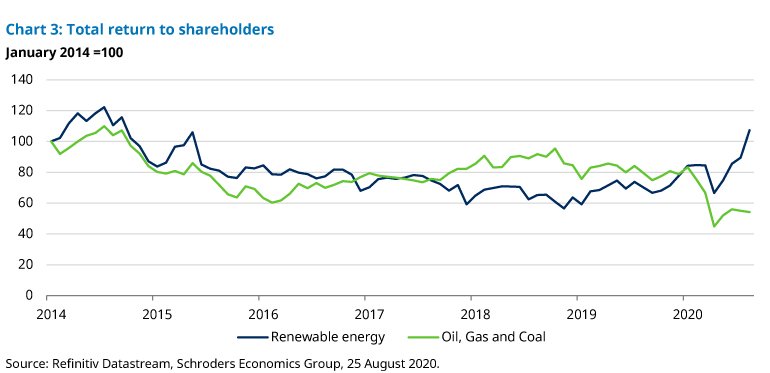

| Carbon dioxide emissions dropped substantially as global economic activity collapsed as a result of the Covid-19 pandemic. However, as emissions tend to move hand-in-hand with macroeconomic activity, the expectation is that they will bounce back as the recovery gathers momentum. The pandemic may have significantly changed the outlook for the oil market. A great deal of comes from the transportation sector and this has been hit dramatically by lockdown measures which brought cars, trucks, trains and airplanes to a standstill. Comments from the airline industry indicate that travel demand will likely remain depressed until there is a vaccine or treatment for the coronavirus. At the same time, long-term structural pressure on the oil industry is likely to stay even when the pandemic eases. Amid concerns about the climate crisis and tighter regulation from governments to control emissions, the oil industry was already under pressure before the coronavirus outbreak. After delivering strong returns at the beginning of the new millennium, the fossil fuel industry started to underperform the S&P 500 in 2014 on the back of plummeting oil prices (chart 1). This trend is likely to continue given the ongoing downward pressure on oil prices from subdued travel demand and a potential shift to cleaner sources of energy such as renewables.  How energy companies are responding to the oil price shock How energy companies are responding to the oil price shock In recent months, we have witnessed several write-off announcements from oil companies, suggesting that oil and gas worth billions of dollars may be left in the ground as a result of lower energy prices. But pressure to decrease carbon intensity and efforts to cut emissions are also playing a role. If this is the case, then even if oil prices recover so that extracting reserves becomes profitable, a large chunk of these assets could be left in the ground. According to the Transition Pathway Initiative (TPI), a global asset-owner led initiative which assesses companies’ preparedness for the transition to a low carbon economy, less than three years ago no European company had set targets to reduce the carbon intensity of the energy it supplied. Today, all companies assessed by the TPI have set such targets. In addition, five major companies (BP, Eni, Repsol, Shell and Total) have recently updated their long-term climate ambitions. Repsol and Total are now aligned with the Paris Pledges scenario, and Shell now plans to cut its emissions intensity by 65% by 2050. As in any challenging transition there will be winners and losers. As pressure on companies to address climate change is only likely to escalate, financial markets should begin to factor in the economic risks of the transition to a low-carbon economy. In particular, any attempt to limit global carbon emissions is going to mean we have to reduce the quantity of fossil fuels we burn. Yet present valuations of energy companies, for example, implicitly assume that their energy reserves have future market value. If this changes, there will be consequences for equity markets. As highlighted in our work on climate change and 30-year market returns, almost 60% of oil and gas reserves, and over 80% of current coal reserves should remain unused in order to limit the increase in global temperature to two degrees Celsius as established in the Paris Agreement. This may result in stranded assets, defined by the International Energy Agency as “those investments which have already been made but which, at some time prior to the end of their economic life, are no longer able to earn an economic return”. Stranded assets is a key risk for markets While oil companies have already written off a substantial amount of fossil fuel reserves in the face of the Covid-induced collapse in energy demand, our analysis highlights that a lot remains in the ground. Risks of a stranded assets scenario have not been priced in. We use MSCI data on companies’ potential emissions to find that the stock markets of countries such as the US, Russia, China and India could see a reduction in returns, should climate policies be implemented in a low carbon transition (chart 2).  As shown by our Climate Progress Dashboard, despite new emissions pledges, we are still far from meeting the Paris target. The pandemic could bring forward the peak of fossil fuel demand and discourage exploration. As shown by our Climate Progress Dashboard, despite new emissions pledges, we are still far from meeting the Paris target. The pandemic could bring forward the peak of fossil fuel demand and discourage exploration. Structural changes are needed to accelerate the transition to a low-carbon economy. Only fiscal and regulatory policy can boost a de-carbonisation of the energy sector through reduced reliance on fossil fuels, increased energy efficiency, and increased use of renewables. According to fDi Markets data, in the first quarter of the year while investment in the oil and gas industry declined dramatically, investment into renewable energy boomed, registering the strongest quarter in a decade. Even more importantly from a financial investor perspective, the renewable energy sector has significantly outperformed the fossil fuel industry since the start of the pandemic (chart 3).  A green recovery could be stronger than a brown one A green recovery could be stronger than a brown one Finally, a green recovery, while being beneficial for the environment and reducing pollution, might prove to be stronger than a recovery in which the bounce back in activity is accompanied by a rise in emissions. Recent research highlights that investment in clean energy creates three jobs for each job lost in the fossil fuel sector, and for each $1m shift from fossil fuels to clean energy, an average of five additional jobs are created. It is important to highlight that this research focussed on the short-term employment effects of reducing fossil fuel production while boosting clean energy production. Therefore, as green energy is a relatively young industry, the decarbonisation of the energy sector is likely to involve significant increases in manufacturing and the installation of renewable and efficiency technologies, providing much needed support to employment at a time where governments try to reboot their economies. |

Brown or green recovery?

Irene Lauro, economist at Schroders, discusses how the pandemic has changed the outlook for the oil industry