On 7 December 2021, while those of us interested in sustainable investing were focused on discussion paper DP21/4 – Sustainability Disclosure Requirements and Fund labels, the Financial Conduct Authority (FCA) published its second consultation paper CP21/13 – a new Consumer Duty.

With this expected to be the biggest change to financial services since RDR in 2012, it’s timely to consider specifically how the measures proposed could affect giving advice on sustainable investments.

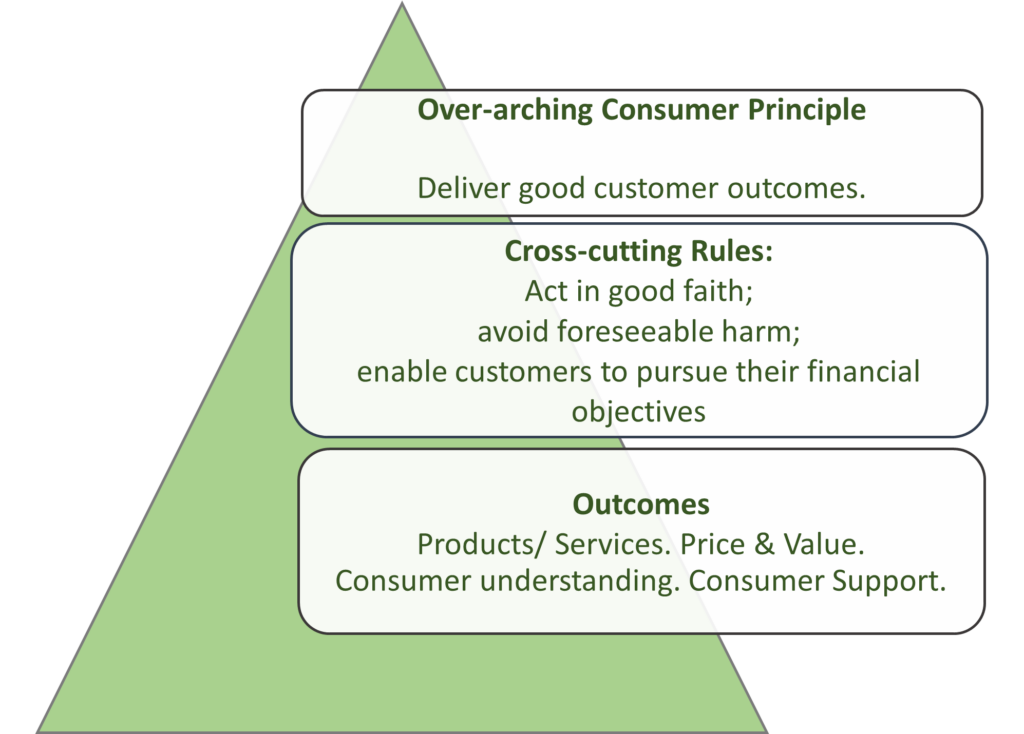

Consumer Duty consists of three tiers, as depicted below:

Advisers can directly relate some of these rules and outcomes to the presentation of sustainable investment products to retail investors.

Enable consumers to pursue their financial objectives

With sustainable investment preferences widely considered to be an important part of an investor’s financial objectives (FCA regulation catching up soon), it’s our consumer duty to ensure that clients are offered every opportunity to pursue these.

See also: – Sustainable investment consultancy launches for advisers

How should we do this?

- Provision of honest and understandable information about the options.

- Time and opportunity to explore and question the client’s needs and wishes.

- Removal of barriers that make a sustainable route more difficult than a non-sustainable one.

Can I suggest a thoughtfully worded, unbiased consumer sustainable investment guide and questionnaire?

Avoid foreseeable harm

This rule references a need to ensure that products and services are fairly described and not cloaked through misleading framing or advertising. Greenwashing certainly springs to mind here.

The harm that could be caused by investing in the wrong type of sustainable investment is potentially different to other types of harm. The customer might not find themselves directly out of pocket or tied to an unfair contract, but disappointment could spoil their confidence in our industry, to the detriment of both parties. Hopefully, the work that has gone into DP21/4 on product disclosures and labels will help us comply with this rule.

The paper also highlights issues relating to “asymmetric information”, a term that refers to “one party in a transaction being in possession of more information than the other”.

I am struck by how relevant this is to conversations between advisers and clients about sustainable investing. Some advisers are apprehensive about being the party who is under-informed if they encounter a client who is personally or professionally interested in environmental and social issues. We must not forget however that personal knowledge of the circular economy or professional expertise in net zero by no means brings any understanding of the investment products that are aligned to these issues.

We will always be the person holding the cards when it comes to understanding how these products work, their aims, opportunities risks and limitation.

Suitable products and services

Providers must be clear of their target market, any risks posed by their products, and also be clear on product information. Distributors must do the same, and take steps to prevent the wrong consumer types from buying/receiving those products.

I can’t pass by this point without raising (again) the problem we have collectively created with the proliferation of ESG – one term, many meanings. Is it a means of:

- Protecting a portfolio against risks.

- Selecting companies that are in an advantaged position.

- Paying the right price for a company, all factors considered.

- Influencing company behaviour.

- Investing in solutions to world problems.

- A combination of some or all of the above?

It doesn’t really matter which of these things an ESG fund is trying to achieve – horses for courses. But Consumer Duty requires that we don’t give an investor ESG type A, if they want ESG type E.

Delivering fair value

Consumers should pay a price for products and services that represents fair value. The FCA notes that this does not mean intervention in pricing but warns that they may have to resort to this if ‘markets are failing to deliver fair value’.

I see a lot of evidence of IFAs worrying abut pressures on the fees they charge – whether from clients who have noted that 1% of £1.5m is £15,000 a year or from the growth of direct-to-consumer competition.

If concerned about challenges to your value for money, then offering a quality sustainable investment proposition is a straightforward way to boost value. It’s a whole new element added to our service and advice proposition. At no additional cost, it can offer clients the following:

- Education on finance, on issues that affect their future and the connection between the two.

- Greater engagement with their finances and their adviser.

- A feeling of satisfaction.

- A sense of individual power and influence and/ or the reassurance of being part of collective change.

- Management of conflicts between their sustainable investment preferences and their financial needs.

Its maybe hard to put a price on that, it’s a very subjective matter, but the FCA says “the level of customer service might justify a higher price.”

Confidence in financial services

The FCA shifts its former emphasis on clear communications to the outcome of consumer understanding. In addition to being fair, clear and not misleading, information must be understandable and facilitate informed consumer decisions.

Fundamentally, I believe we need to look at every investment, process and communication on sustainable investing through a consumer lens. We constantly need to ask if the things that we like or dislike about a product will match the end investor’s likes, dislikes, understanding and intention.

There’s a lot of work to be done on the information and processes we currently deliver in relation to sustainable investing – both to facilitate consumer understanding and our understanding of the consumer.

I’m pretty glad I’ve made this my focus and am here to help where IFA firms feel they need support in this area.

Dates for the diary

Second consultation period closes 15 February 2022

FCA to publish responses and new rules July 2022.

Firms expected to implement these by April 2023.